I’m a sucker for “innovation at the edges,” and healthcare is loaded with edges. When you run a company with under 25 employees, you don’t need another think piece, you need a field guide that respects your time and your budget. I have put together an unvarnished view of what is changing, why it matters, and how to play the next 12-24 months without turning benefits into your second job.

Plot twists that actually matter

Healthcare is being re-priced in real time, all the time. Premiums keep grinding up while the system invents new ways to bill you for “value”. The line is still heading up and to the right, even if you have already done the obvious cost-containment strategies that you have heard about.

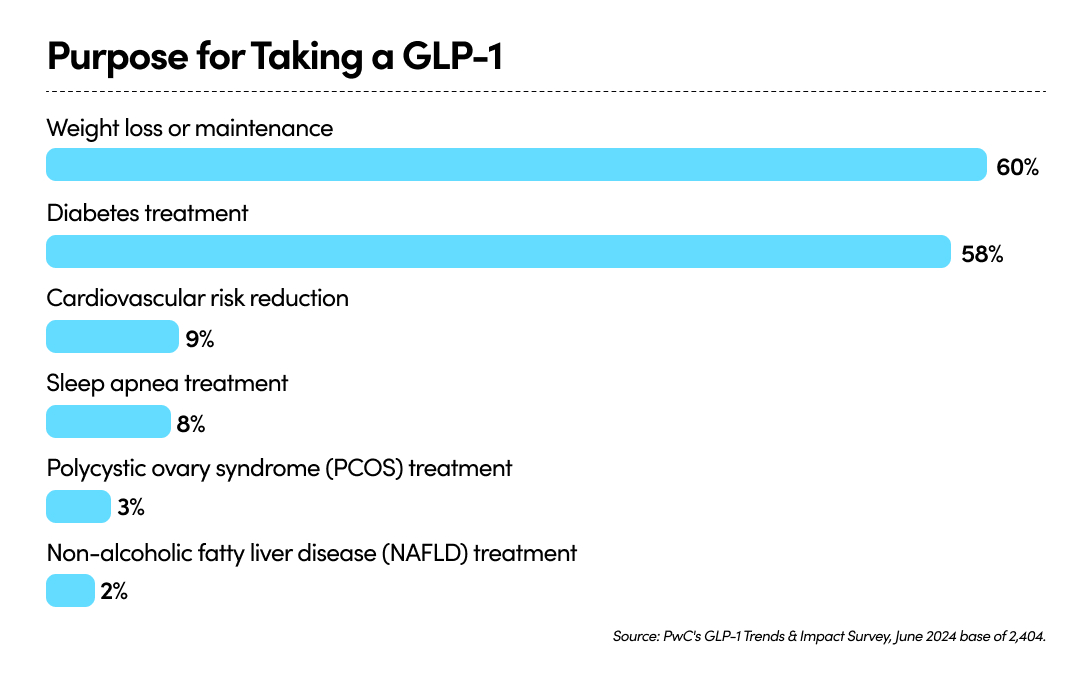

GLP-1s transformed pharmacy economics, and extensive clinical data shows these drugs work well across multiple therapeutic areas (see graph below). The reality is, when demand for something this successful keeps increasing, so does the cost. Left unmanaged, a single drug class can quickly hijack spend for any small group. Plans are experimenting with clinical guardrails, outcomes agreements, and coverage carve-outs. Translation: volatility. I will write an entire article on this in the future, but felt it was worth mentioning due to how much of an outlier GLP-1s have become.

Transparency is finally acquiring teeth. Price files are going from theoretical to usable. As the data hardens, expect more steerage to high-value providers and cash-pay bundles. That is leverage you can use, if you are set up to use it—more on that later.

Funding is drifting down-market. Level-funded, reference-based pricing, and small-group captives are creeping into the sub-50 employee space. Not a silver bullet, but it is expanding the playbook beyond “praying for a cheap renewal”. Historically, these cost-containment measures were only available to large organizations with buying power, but today technology is making it easier to bridge this gap and provide strategy to smaller companies.

The Healthcost Paradox

In recent years we’ve seen significant shifts in receiving better care, earlier diagnoses, smarter drugs, fewer catastrophic events, and the bill still rises. That’s the Healthcost Paradox: efficiency collides with a labyrinth distribution system. Every layer (Pharmacy Benefit Managers, carrier admin, provider facility fees, navigation platforms, brokers, reinsurance etc.) takes a cut or adds friction. In most markets, efficiency drops the price. In U.S. healthcare, efficiency often increases utilization, expands eligibility, and then runs headfirst into a basic economics problem: we have constrained supply and subsidized demand; i.e., there are only so many doctors, yet demand on their skill is relatively unlimited and innovation shortens the timeline to access them.

"The worsening clinical labor shortage is a significant contributor to our projected increase in healthcare costs over the next five years." — McKinsey & Company

This paradox leaves small teams vulnerable. While the system grows more complex, they’re expected to navigate it with fewer resources. The good news is that there is a practical playbook for taking control.

A simple playbook for teams under 25 employees:

- Treat benefits like a product and not a line item. Set a “medical budget” you’re willing to sustain over the next 24 months, then build a roadmap: what you will add, what you will retire, and what success means (claims avoided, retention improved, time-to-care shortened). If a benefit can’t prove it moves one of those, it’s a nice idea but not a priority.

- Decide your GLP-1 policy before renewal. Practical stance: cover for diabetes; consider anti-obesity coverage with clinical criteria, step therapy and maintenance requirements; pair access with coaching and nutrition. And please, push for outcomes-based pharmacy terms where possible. Be deliberate in the goal: better health.

- Weaponized transparency. Ask your broker or benefits administrator to turn price files into action: identify shoppable services with price variance. Negotiate, or hire someone to methodically negotiate on your behalf, a better option for you. This can be done and most American healthcare consumers either do not know how or do not have the time. Billing departments have little incentive to bill you less unless there's pushback.

- Design to avoid out-of-network landmines. Tighten referral rules, verify provider network status at scheduling, and give employees a hotline when something looks off. Every avoided arbitration is money and time you keep.

- Communicate like a startup. I have a bit of bias here, but startups are about speed. The healthcare system is not. You need two pages, quarterly: what has changed, why has it changed, how can you use it, and where to get help. No jargon or PDFs from 2017. People will use benefits correctly if you make “correct” stupid simple.

The One Big Beautiful Bill Act (OBBBA): what matters for small teams.

- Marketplace subsidies are set to shrink at year-end 2025 unless Congress acts. Enhanced ACA premium tax credits expire after 2025, which means Marketplace-reliant employees (think: part-timers, lower-wage workers, or teams using ICHRA) could face higher net premiums in 2026. Plan for churn and affordability conversations.

- Medicaid rules tighten. New work reporting requirements, more frequent redeterminations, and immigration-eligibility changes will mean coverage losses over the next decade. Translation for small employers: more candidates and employees bouncing between coverage sources and more demand for simple, predictable options.

- Household cash flow shifts from tax changes. Separate from health provisions, OBBBA’s “no tax on tips/overtime” and other deductions will adjust take-home pay. Good to know as you calibrate employee contributions and wage-benefit tradeoffs.

Net-net: OBBBA widens HSA+ strategies while raising the odds of coverage churn in Medicaid/Marketplace populations. If you rely on ICHRAs, revisit your 2026 contributions and communications now. If you're a fully insured small group, test whether a level-funded or captive path plus a clean HSA strategy would put you ahead of the 2026 curve.

Where this is all heading

Simply put, if healthcare costs remain unchecked in the United States, healthcare will crumble. Don’t try to solve the nation’s healthcare. Solve your healthcare. I recommend you choose two moves you can execute cleanly in the next quarter, then measure the impact, and iterate. This is how startups beat larger incumbents: tight loops and quick action.

If you’re staring at a renewal you’ll need to pivot differently. If one drug class is eating your budget, you’re not uniquely cursed, you’re experiencing the system as designed.

The opportunity in this messy, shifting marketplace, is to design a system that routes around the friction and buys outcomes, not theatrics.

That's the drum I beat at Meridio: a partner for affordable healthcare for growing businesses. Not a magic wand, not a lecture. Just a disciplined way to structure buying, managing, and communicating benefits so small business owners can get the same leverage as large companies.

— Bobby Sain, Meridio CEO

Ready to Explore Your Options?

If you are a business owner with a small or fast-growing team looking for a simpler, more supportive way to offer health benefits, it may be time to see if Meridio is the right fit. Schedule a conversation with our team to learn more.

Latest Posts

Finally, Health Benefits That Make Sense for Franchise Businesses

Evaluating the Right Health Benefits Path for Your Operations